A Letter to CBSE Accountancy Class XII Board Exam Students

Dear Students,

As you prepare to appear for your CBSE Accountancy Class XII Board Examination, I want to remind you of a few important points that will help you perform your best.

Dear Students,

As you prepare to appear for your CBSE Accountancy Class XII Board Examination, I want to remind you of a few important points that will help you perform your best.

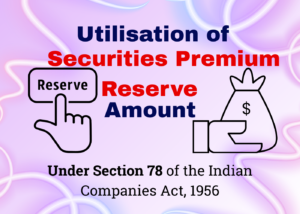

When a company issues shares at a premium (for example, a share of face value ₹10 issued at ₹12, i.e., ₹2 premium), the extra amount collected is credited to the Securities Premium Reserve Account.

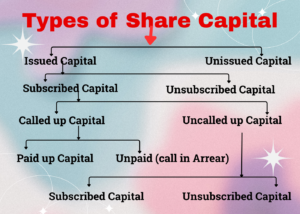

Share Capital is the amount of money a company raises by issuing shares to the public (shareholders). It represents the ownership money invested in the company by shareholders.

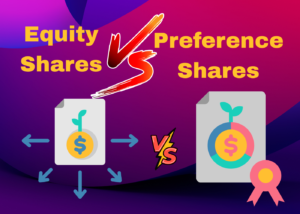

A share is a unit of ownership in a company. If you buy shares, you become a shareholder and get rights like receiving dividends and voting in company matters.

Imagine a large company as a giant pie. A “share” is a single slice of that pie. When you purchase a share, you are buying a defined fraction of ownership in that company. This ownership status, known as being a shareholder, comes with specific privileges. These can include a potential claim on a portion of the company’s profits and a voice in major company decisions.

Dear Students, As you prepare to appear for your CBSE Accountancy Class XII Board Examination, I want to remind you of a few important points that will help you perform your best.

Every year, lakhs of CBSE students leave the exam hall saying the same thing: 👉 “The paper was easy… I just couldn’t finish on time.” What most students don’t realise is this: Your board exam...

My Kid is Writing the Exam, But I’m the One Holding My Breath.