Fixed Capital vs. Fluctuating Capital

Unique Learning Academy

16/03/2026

Accountancy XII

Class 12,

Accounting for Partnership Firm – Fundamentals

Partnership Accounting: Fixed Capital vs. Fluctuating Capital

In a partnership business, separate capital accounts are maintained for each and every partner. All transactions of the partners — including the amount contributed as capital, withdrawals (drawings), share of profit or loss, interest on capital, interest on drawings, partners’ salary, and commission — are recorded through their capital accounts.

The capital accounts of partners may be maintained in two ways:

- Fixed Capital Accounts

- Fluctuating Capital Accounts

⭐ Important Note: In the absence of any specific instruction, the capital account should always be prepared using the Fluctuating Capital Method by default.

(A) Fixed Capital Accounts — “Keep My Investment Separate, Please”

Imagine you and your friend start a business. You put in ₹5,00,000 as your capital. Under the Fixed Capital Method, that number stays locked. Year after year, your capital account shows ₹5,00,000 — unless you both formally agree to add more or take some out permanently.

But wait — what about your salary from the firm? Your share of profit? The interest on your drawings? Where do all those go? They go into a separate account called your Current Account.

When the original capitals invested by the partners do not change and remain constant, unless some additional capital is introduced or some amount of capital is withdrawn under an agreement, this type of capital account is called a Fixed Capital Account.

All entries related to share of profit or loss, interest on capital, interest on drawings, salary, commission, and personal withdrawal (drawings) are recorded in a newly-opened account for each partner — named the Current Account.

When partners maintain fixed capital accounts, the following two accounts are prepared separately:

Partners’ Capital Account will always show a credit balance, which shall remain the same (fixed) year after year, unless there is any addition or withdrawal of capital. Partners’ capital accounts shall always appear on the Liabilities side of the Balance Sheet.

- Debit side records: Permanent withdrawal of capital and closing balance (Balance c/d).

- Credit side records: Opening balance (Balance b/d) and any additional capital introduced (Cash/Bank).

Partners’ Current Account may show either a debit or a credit balance.

- If the current account shows a credit balance, it is shown on the Liabilities side of the Balance Sheet.

- If it shows a debit balance, it is shown on the Assets side of the Balance Sheet.

Debit side entries: Opening debit balance (if any), drawings, interest on drawings, and share of loss.

Credit side entries: Opening credit balance (if any), interest on capital, salary, commission, and share of profit.

(B) Fluctuating Capital Accounts — “Just Put Everything in One Place”

Now imagine you’d rather keep things simple. No separate current account. Just one account per partner, and everything goes straight into it — your drawings, your profit share, your interest, your salary, all of it. That’s the Fluctuating Capital Method.

Because everything flows in and out of the same account, the balance keeps changing — or fluctuating — from year to year. One year it might be ₹6,00,000. Next year ₹4,50,000. It depends entirely on what happened during the year.

And yes — if you drew out more than you earned, your account could actually show a debit balance, meaning you owe money to the firm.

Sometimes the original capital invested does not remain the same and keeps on changing from year to year. This happens because all entries related to profit or loss, drawings, interest on capital, salary, etc., are directly recorded in the capital accounts of the partners. This makes the balance fluctuate from time to time — hence it is called the Fluctuating Capital Account.

Under this method, only one account (i.e., the capital account) is maintained for each partner. There is no separate current account.

- Debit side entries: Drawings, interest on drawings, and share of loss.

- Credit side entries: Opening balance, additional capital, interest on capital, salary, commission, and share of profit.

⚠️ Debit Balance Warning: Under the Fluctuating Capital Method, if a partner’s total drawings and allocated losses exceed their capital and earnings, the account can show a debit balance — meaning the partner effectively owes money to the firm.

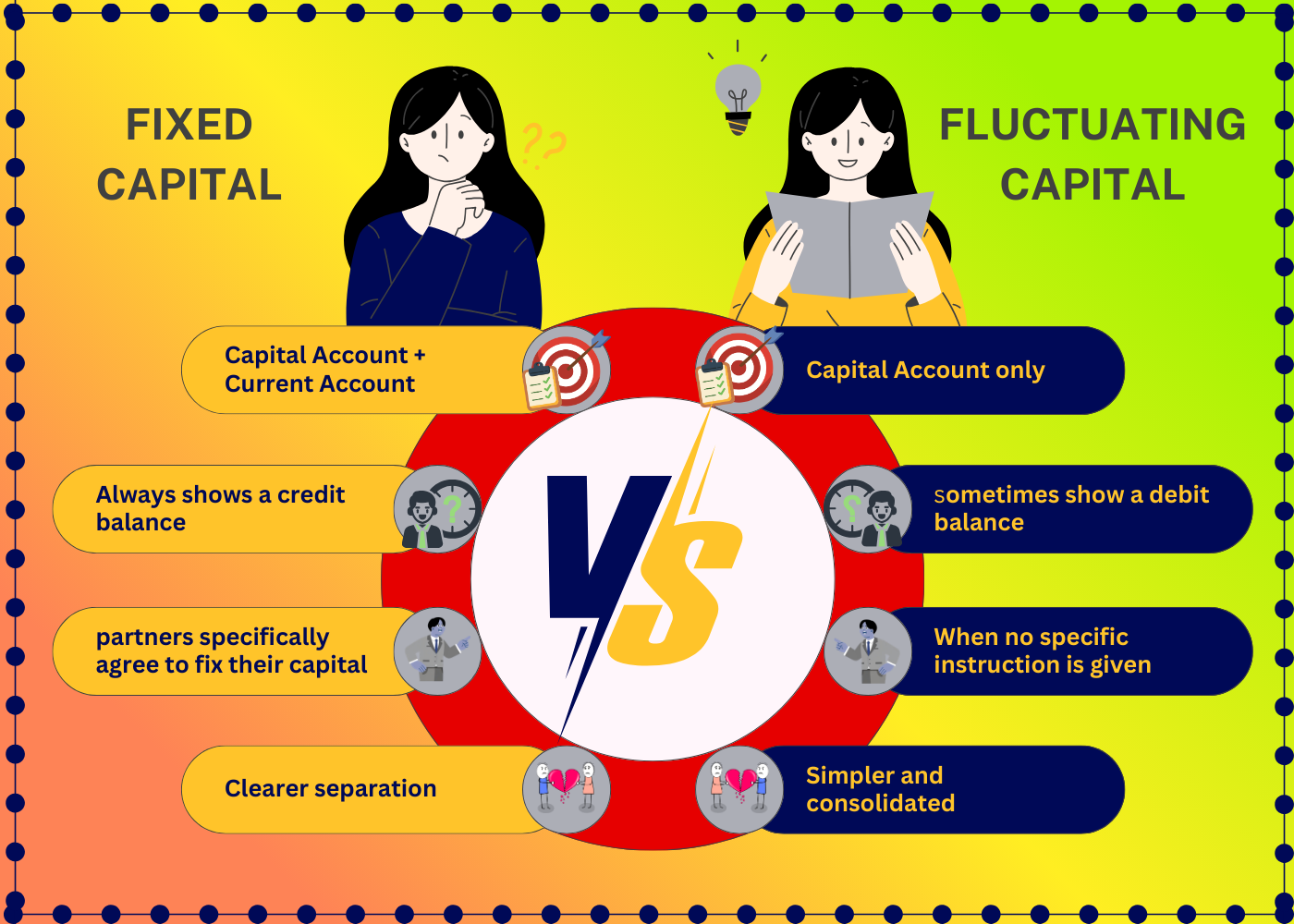

Distinction Between Fixed and Fluctuating Capital Accounts

| Basis | Fixed Capital Account | Fluctuating Capital Account |

|---|---|---|

| Number of Accounts | Two per partner — Capital Account + Current Account | One per partner — Capital Account only |

| Adjustments | All adjustments recorded in the separate Current Account | All adjustments recorded directly in the Capital Account |

| Balance Stability | Capital balance remains constant year after year | Balance fluctuates frequently from year to year |

| Credit/Debit Nature | Capital Account always shows a credit balance | Capital Account may sometimes show a debit balance |

| Complexity | Two accounts per partner — clearer separation but more records | One account per partner — simpler and consolidated |

| Default Usage | Used only when partners specifically agree to fix their capital | Applied by default when no specific instruction is given |

Which Method Should You Use?

The choice between fixed and fluctuating capital depends largely on the partnership agreement and the partners’ preference for record-keeping.

Fixed Capital Method: Ideal when partners want to maintain a clear, permanent record of their original investment, separate from routine income and expense adjustments. It provides greater clarity and transparency.

Fluctuating Capital Method: Preferred when the partnership wants simplicity, with a single account absorbing all transactions. It is also the method applied by default when the partnership deed is silent on the issue.

Both methods ultimately arrive at the same net result — they simply differ in how they organise the information. Understanding both is essential not just for examinations, but for reading and interpreting partnership financial statements accurately.

Quick Rule to Remember: If the exam question doesn’t mention which method to use — always go with the Fluctuating Capital Method. That’s the default.

Key Takeaway

Partners’ capital accounts are more than just accounting entries — they are the financial mirror of each partner’s stake in the business. Whether fixed or fluctuating, maintaining them correctly ensures transparency, fairness, and accuracy in the firm’s books.

- Fixed capital keeps things steady and structured, with a dedicated current account absorbing all adjustments.

- Fluctuating capital keeps things simple and consolidated, with all transactions flowing through a single account.

- Knowing the difference — and knowing when each applies — is a foundational skill in partnership accounting.

Unique Learning Academy

Gurugram

Have Any Question?

Wish to enquire about our teaching pedagogy? Contact Us via Call or Email

- +91-9136-336-336

- contact@uniquelearning.in

Have Any Question?

Wish to enquire about our teaching pedagogy? Contact Us via Call or Email

- +91-9136-336-336

- contact@uniquelearning.in